Die verborgenen Mechanismen hinter dem Bonus-Timing

In der privaten Vermögensverwaltung konzentrieren sich die Vergütungsdiskussionen oft auf absolute Zahlen, wie z. B. die Aufteilung der Einnahmen, Hürden und Aufschübe. Eine Dimension, die jedoch selten öffentlich diskutiert wird, ist der Zeitpunkt. Wann Boni gezahlt werden - ob vierteljährlich oder jährlich - kann sich erheblich auf die Moral der Mitarbeiter, die Liquidität, das Vertrauen und die strategische Ausrichtung auswirken.

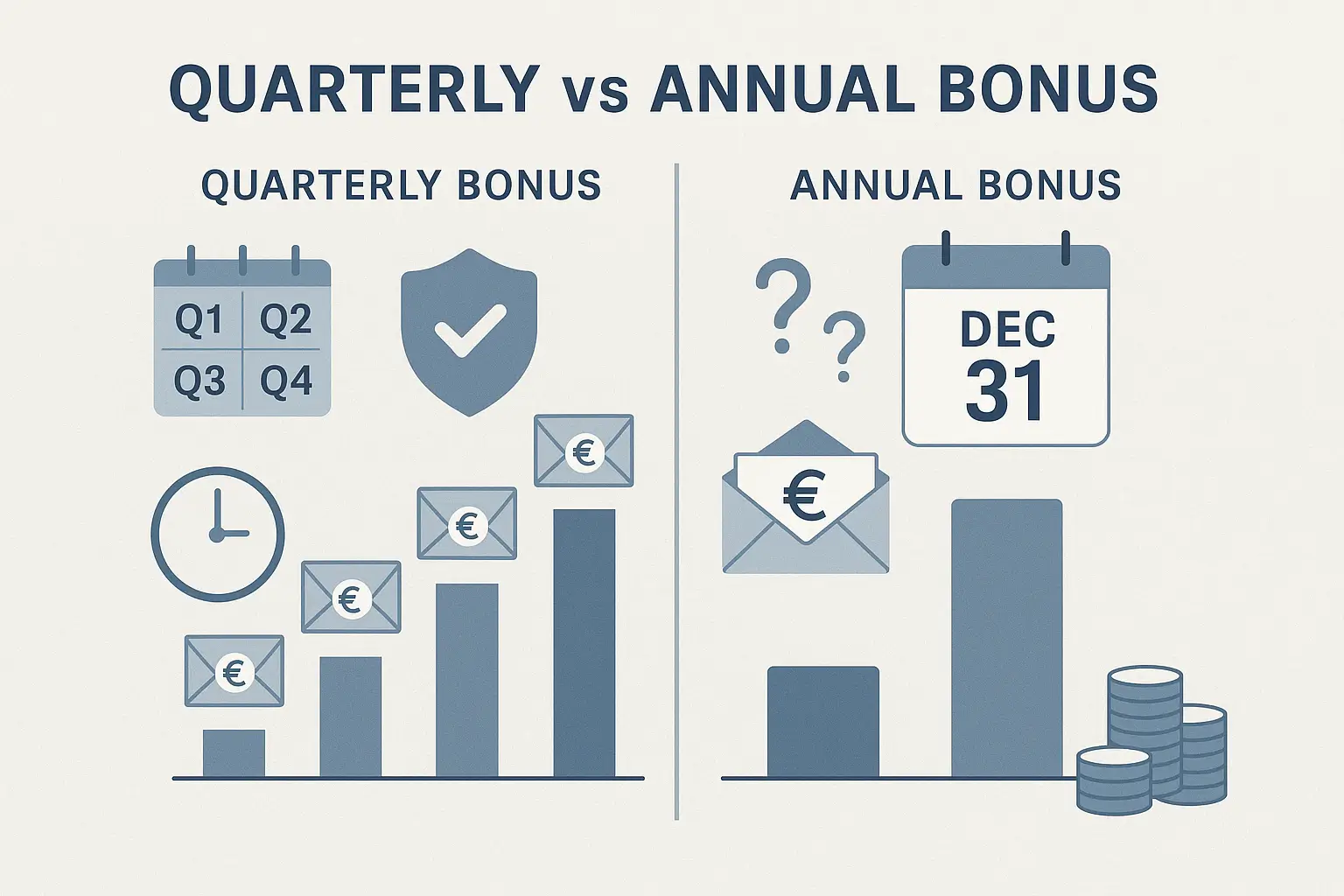

Traditionell werden die jährlichen Auszahlungen sind die Norm gewesen. Sie erlauben Management um die Leistung ganzheitlich zu bewerten, die Dynamik zwischen den Abteilungen zu berücksichtigen und die Gesamtkosten besser vorhersehbar zu steuern.

Aber diese Struktur bringt implizite Nachteile mit sich. Viele Berater kennen den Dezember Bonus Gespräch zu gut: "Großartiges Jahr - aber andere Abteilungen haben unterdurchschnittlich abgeschnitten." Das Ergebnis? Eine geringere Auszahlung trotz erheblicher individueller Beiträge. Diese Schieflage untergräbt das Vertrauen.

Vierteljährliche Boni bieten dagegen eine größere Detailgenauigkeit. Sie ermöglichen es den Unternehmen, Beiträge zu belohnen, die näher an dem Zeitpunkt liegen, an dem sie erbracht werden, und so Aufwand, Anerkennung und Geldfluss in Einklang zu bringen. In einem schnelllebigen Beratungsumfeld ist das wichtig.

Timing, Liquidität und die versteckte Rendite aufgeschobener Ausschüttungen

Vierteljährliche Bonusmodelle bieten weniger Möglichkeiten zur Renditeoptimierung als die durch gestaffelte Erträge finanzierten Jahresendauszahlungen. Dennoch gibt es einen messbaren Effekt.

Angenommen, ein Unternehmen erwirtschaftet 1,25 Mio. CHF in fee-abhängiges Einkommen pro Quartal, wobei jährlich 5 Millionen CHF für Boni vorgesehen sind. Im Rahmen eines jährlichen Auszahlungsmodells werden diese vierteljährlichen Einnahmen jährlich akkumuliert und können in kurzfristige Einlagen investiert werden, solange sie gehalten werden.

Bei einer jährlichen Rendite von 1,25% würde diese Struktur etwa 23.437,50 CHF an Zinsen pro Jahr einbringen. Die Logik: Die Erträge aus Q1 werden 9 Monate lang gehalten, Q2 6 Monate lang, Q3 3 Monate lang, und Q4 wird direkt ausgezahlt.

Bei vierteljährlichen Auszahlungsmodellen hingegen werden die Erträge auf der Grundlage der Leistung verteilt. Sie eliminieren diese Zinsspanne, schaffen aber Vertrauen, Transparenz und Bindungsvorteile, die viele Institutionen als wertvollere Rendite ansehen.

Für den Relationship Manager: Gewissheit und Bindung

Aus der Sicht des Beraters bietet die vierteljährliche Vergütung psychologische und finanzielle Vorteile. Sie verringert die Unsicherheit, unterstützt die Planung und bietet ein gewisses Maß an Sicherheit, dass die Leistung in Echtzeit beurteilt wird und nicht am Jahresende aufgrund von Faktoren, die außerhalb der eigenen Kontrolle liegen, neu kalibriert wird.

Dadurch wird die Notwendigkeit langfristiger Anreize oder Aufschübe nicht außer Acht gelassen. Es schafft jedoch einen stabileren Einkommensrhythmus, was besonders für unabhängige Manager oder leitende Bankangestellte wichtig ist, die als Unternehmer innerhalb einer regulierten Plattform tätig sind.

Für Kunden: Ein subtiler, indirekter Gewinn

Kunden fragen vielleicht nie, wie der Bonus ihres Beraters strukturiert ist. Aber sie spüren die Konsequenzen.

Ein Manager, der nicht weiß, wie er am Jahresende dasteht, ist eher geneigt, Entscheidungen hinauszuzögern, kurzfristige Zahlen zu schützen oder sich bei Unsicherheit zurückzuziehen. Vierteljährliche Systeme fördern eine kontinuierliche Rechenschaftspflicht - und oft auch einen präsenteren, proaktiven Berater.

Dieser subtile Vorteil kann in unabhängigen Unternehmen, in denen das Vertrauen der Kunden die eigentliche Währung ist, zu längeren Geschäftsbeziehungen und besserer Beratung führen.

Strategische Implikationen

Es gibt kein perfektes Modell. Jährliche Auszahlungen bieten strategische Kontrolle, während vierteljährliche Boni die Reaktionsfähigkeit in den Vordergrund stellen. Ein hybrider Ansatz - vierteljährliche Vorauszahlungen mit Anpassungen am Jahresende - kann das Beste aus beiden Welten bieten.

Letztendlich spiegelt der Zeitplan für Boni die institutionelle Kultur wider: Kontrolle versus Autonomie, Standardisierung versus Flexibilität.

Unternehmen, die dies verstehen, optimieren nicht nur ihre Vergütung. Sie signalisieren damit, wer sie sind - und wie sie über Menschen denken.

Weitere Lektüre zum Thema Vergütung und Anreize

- Vergütungsmodelle für Vermögensverwalter

- Bankenboni: USA und Europa - Trends und Spannungen

- Mehr als AUM: Wie unabhängige Vermögensverwalter ihren Erfolg messen

- Kompensation als Beziehungssignal

- Preisgestaltung von Beratungs- und Ermessensmandaten